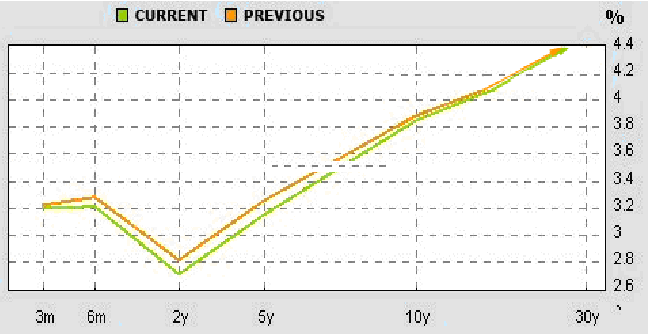

excel yield curve_current yield是什么_yield curve(3)

电脑杂谈 发布时间:2017-06-07 21:04:37 来源:网络整理I will illustrate the calculations on the example below. The parameters are in cells A44 (underlying price), B44 (strike price), 4 (volatility), D44 (interest rate), E44 (dividend yield), and G44 (time to expiration as % of year).

Note: It is row 44, because I am using theBlack-Scholes Calculator for screenshots. You can of course start in row 1 or arrange your calculations in a column.

When you have the cells with parameters ready, the next step is to calculate d1 and d2, because these terms then enter all the calculations of call and put option prices and Greeks. The formulas for d1 and d2 are:

All the operations in these formulas are relatively mathematics. The only things that may be unfamiliar to some less savvy Excel users are the natural logarithm (LN Excel function) and square root (SQRT Excel function).

The hardest on the d1 formula is making sure you put the brackets in the right places. This is why you may want to calculate individual parts of the formula in separate cells, as I do in the example below:

First I calculate the natural logarithm of the ratio of underlying price and strike price in cell H44:

=LN(A44/B44)

Then I calculate the rest of the numerator of the d1 formula in cell I44:

=(D44-E44+POWER(4,2)/2)*G44

Then I calculate the denominator of the d1 formula in cell J44. It is useful to calculate it separately like this, because this term will also enter the formula for d2:

=4*SQRT(G44)

Now I have all the three parts of the d1 formula and I can combine them in cell K44 to get d1:

本文来自电脑杂谈,转载请注明本文网址:

http://www.pc-fly.com/a/tongxinshuyu/article-51683-3.html

上海市普陀区电子设备的销毁-不合格计算机配件的销毁处理

上海市普陀区电子设备的销毁-不合格计算机配件的销毁处理 有关电力谐波的论文的参考文献在哪里可以找到有关电力谐波的英语参考文献

有关电力谐波的论文的参考文献在哪里可以找到有关电力谐波的英语参考文献 如何为扫地机器人充电

如何为扫地机器人充电 无线激光条码采集器_seuic 条码采集器_无线条码扫描器使用

无线激光条码采集器_seuic 条码采集器_无线条码扫描器使用

唉你哦